The high-yield properties in good locations sought by Swiss and foreign investors are unlikely to come on the market at reasonable prices, with the consequence that investors are interested in new projects, rather than existing properties in need of renovation.

Until now this area was mainly the province of local architects, as well as general and specialized contractors. As a rule they offer new projects to Swiss institutional investors at an all-inclusive price, set completion date, specifications and yield, the latter at times with rental income guarantees attached.

As is increasingly evident at international real estate fairs such as MIPIM in Cannes and ExpoReal in Munich, foreign investors develop their own projects, know what they are looking for and are well versed in project development and construction.

CIL law limits investment opportunities

As regards ownership, CIL, the federal law on collective capital investment (Collective Investment Schemes, CISA), in particular Art. 86 para. 4 of the Collective Investment Schemes Ordinance (CISO), put severe limitations on project development: Undeveloped land without infrastructure and not immediately open to development may not be purchased.

Weitere Informationen zum Thema Immobilienentwicklung finden Sie hier:

[spoiler effect=”slide” show=”Foreign project developers” hide=”Foreign project developers”]

Foreign project developers

Project organization and great knowledge of project management notwithstanding, most foreign project developers or direct investors lack:

- local market and construction industry know-how

- knowledge of Swiss law

- familiarity with the Swiss way of thinking, doing things and negotiating.

[/spoiler]

[spoiler effect=”slide” show=”Change monitoring” hide=”Change monitoring”]

Change monitoring

Project developers seeking development opportunities keep a close watch on zoning and population situations.

[/spoiler]

[spoiler effect=”slide” show=”Initiating a project” hide=”Initiating a project”]

Initiating a project

This document addresses

- (foreign) investors who seek property investment opportunities

- (foreign) developers seeking to buy land for new projects.

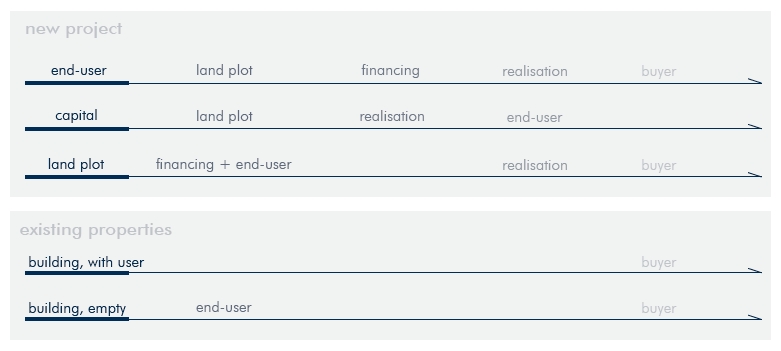

A project may also have an external trigger (see box Ideal and less-than-ideal scenarios, below).

Ideal and less-than-ideal scenarios

- Ideally, a project developer has an end-user seeking land.

- The user’s existence opens the door to outside financing.

- The second-best scenario is a project developer with an institutional investor lined up who is intent on making an investment.

- This raises two questions :

- lack of end-users

- facilitation of a closing by means of a rental income guarantee issued to the investor

- limited yield potential as a rule.

- lack of end-users

- This raises two questions :

Projects for which the developer has to secure capital and end-user are accordingly more demanding and costly.

Project trigger:

Click on image to view full size

[/spoiler]

[spoiler effect=”slide” show=”Project concept, intrinsic value” hide=”Project concept, intrinsic value”]

Project concept, intrinsic value

To give intrinsic value to a project, the investor or developer must able to

- have a project concept

- find the required land

- have end-users

- secure the capital (equity and/or outside capital).

Checklist

The project developer collects, processes and evaluates data, assesses plausibility (project analysis) and interprets the results (synthesis).

These tests apply:

- Can the project be realized as planned?

- Is it viable financially now as well as long term?

- Can financing be secured?

[/spoiler]

[spoiler effect=”slide” show=”Overview” hide=”Overview”]

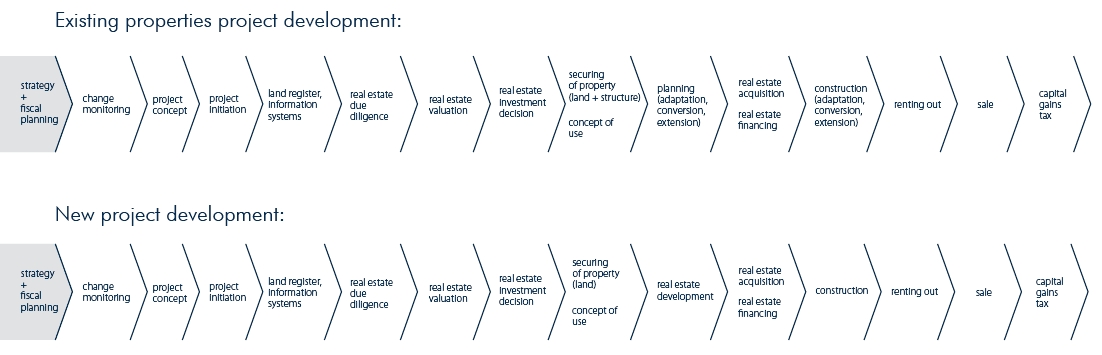

Overview

Project development from purchase to sale is different for existing properties and for new projects:

Click on image to view full size

[/spoiler]

[spoiler effect=”slide” show=”Real estate project” hide=”Real estate project”]

Real estate project

The real estate development process consists of

Kinds of development

- existing buildings (conversion, extension)

- new constructions

Alterations of existing vuildings (pursuant to SIA Standard 469)

- conversion

- to improve comfort level

- to meet new regulations

- to raise load-bearing capacity

- to meet changed requirements

- extension

- by means of an addition

- adding another floor

- enlargement.

Development process

In Switzerland real estate development ideally proceeds as follows:

- strategic planning

- project organization

- preliminary studies

- project definition

- floorspace

- gross leasable (rent and revenue generating) area (GLA)

- floor space (FS) as per building regulations

- ratio of GLA to FS

- projected yield

- long-term yield on investment

- IMPORTANT:

- different expressions of yield

- valuation

- static yield

- dynamic yields

- discounted cash flow method

- economic value-added method

- internal rate of return method

- payback method

- rental law

- net return (OR 269, Swiss Code of Obligations)

- cost-covering gross yield (OR 269a lit. c, Swiss Code of Obligations)

- valuation

- terms differ from country to country (see Real estate valuation, above)

- different expressions of yield

- floorspace

- feasibility study

- selection process

- project definition

- project planning

- preliminary project

- construction project

- building permit application (the required paperwork)

- bidding process (bid submission and award )

- implementation

- execution planning

- execution

- taking over property and commissioning

- correcting defects

- final account

Property acquisition (land or land plus buildings)

Unless the project developer, or active investor, secures a property he runs the risk of project planning becoming redundant should the site be sold to someone else. Securing property in advance is an imperative.

- reservation agreement

- purchase right

- purchase contract

Property acquisition has tax implications, even if the real estate developer only concludes a property purchase agreement with a right to contract on behalf a third party, and after the contract comes into force the third party subsequently acquires the development site.

Contract of sale

Development projects usually entail great material, economic and financial risks, which makes foresight and in-depth examination of the contract doubly important:

- property purchase agreement

- including a rescinding or resolutory condition

- building permit

- partially rented

- financing

- etc.

- warranty

- inclusion of real estate due diligence results

- environmental aspects

- assurances regarding projected use

- including a rescinding or resolutory condition

- architectural and planning contract

- performance specifications

- budgeting liability

- contracts for services

- performance guarantee

- mandatory warnings

- soil and subsoil risks

- performance-linked, flat-rate payments

- performance guarantees and security provision

- rental agreements with end-users

Further information:

» praeventionsberatung.ch (in German)

» reservationsvereinbarung.ch (in German)

» industriebrache.ch (in German)

» Contaminated site or abandoned hazardous site?

» zwischennutzungen.ch (in German)

[/spoiler]

[spoiler effect=”slide” show=”Project financing” hide=”Project financing”]

Project financing

These criteria determine availability of financing:

- developer-owned project

- site owner

- project financing assured with property as security

- project financing can usually be secured when project details are promising

- lack of site

- project helps sell a contractor’s or general contractor’s contract and serves as investor decision-making basis based on development criteria such as surface area and yield

- if the project itself offers no security in and of itself, financing is doubtful

- site owner

- commissioned project

- An owner’s pre-payments, down or partial payments have security potential in the form of security assignment, right of attachment, etc., which makes them relevant to outside financing.

- Swiss banks approach project financing very conservatively.

[/spoiler]